2023 Closing Review

An overview of the crypto industry landscape for 2023: L1 and L2 stress test, LPDFi, LSDFi, RWA.

Disclaimer: The content presented in this article, along with others, is based on opinions developed by the analysts at Dewhales and does not constitute sponsored content. At Dewhales, we firmly adhere to a transparency-first philosophy, making our wallets openly available to the public through our website or DeBank, and our articles serve as vehicles for self-expression, education, and contribution to the ecosystem.

Dewhales Capital does not provide investment advisory services to the public. Any information should not be taken as investment, accounting, tax or legal advice or as a recommendation to purchase, sell or hold or to pursue any investment style or strategy. The accuracy and appropriateness of the information is not guaranteed by Dewhales Capital.

Introduction

1. 2023 is a Year of Liquid Solutions

2. LSDFi

3. Stress Testing Chain Resilience through Inscriptions

4. Bridgeless Future of 2024

5. Intertwining RWAs, Blockchain and Web3 Markets

5.1 Perspective 1: Web3 Markets’ Adoption of RWAs

5.2 Perspective 2: RWAs’ Adoption of Public Blockchains

5.3 Perspective 3: Investor Interest and Liquidity

6. Looking Forward To 2024 For RWAs

Conclusion

Introduction

The passing year of 2023 has been quite an exciting and extreme journey, another crazy year in crypto. The market went through many stages that the crypto industry is so loved for: from updating the BTC low at the very beginning of 2023 to its rise at the end of the year and the launch of various narratives: Ethereum Shapella hardfork, the formation of LSDFi with its dramas and hopes, meme coins, inscriptions, the active acceleration of the RWA narrative, the rebirth of Solana from the ashes, waiting for ETF approval and many other different trends and events.

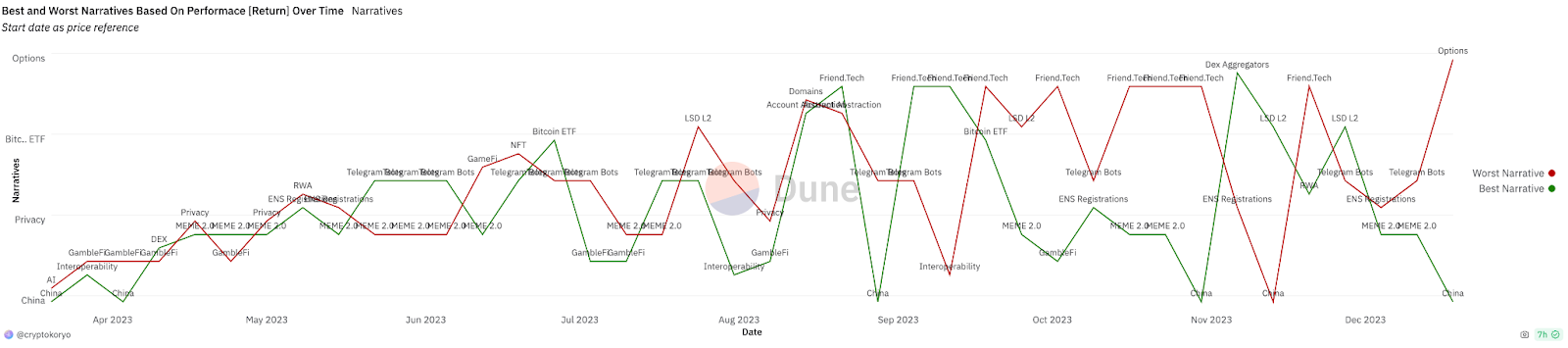

Undoubtedly the meme coins trend left a big mark this year, but there were also other trends such as AI, the surge in popularity of perp dexes, the launch of the hype around SocialFi with Friends.tech, successful launches of TG trading bots and so on. And each of these individual trends can be considered significant, and each of them had their time. But if we look at a graph of the popularity of those particular trends, we don't really see any strongly pronounced peaks over a long period of time. Rather, they've been intermittently successive.

It can probably be compared to driving in traffic on a broadband road: most of the time, the driver thinks the neighbouring row is starting to go faster, they move to another row and instead the row the driver was in before starts going faster. But there are drivers who manage to catch the rhythm and move faster than the flow, rearranging from row to row, but this is usually an exception to the general mass.

So in our review of the past year, we won't focus on temporary things that are replaced by other things. Instead, we will try to look at the overall picture of the state of the crypto industry, how it has changed in terms of the state of the infrastructure, how successful the global long-term processes are, and what groundwork is being laid for the future. After all, hype things are made possible precisely because of the development of infrastructure and the emergence of new underlying protocols and products. So we will focus on things like LSDFi, a review of the state of blockchains and RWA.

1. 2023 is a Year of Liquid Solutions

In 2023, at Dewhales, our primary focus revolved around liquid staking tokens (LSDfi) and liquid providing derivatives (LPDfi). We published four major articles delving into the intricacies of LSDfi and LPDfi.

In our initial article, we conducted a comprehensive analysis comparing LSD with conventional staking. We elucidated the impact of the Ethereum Shanghai update on this process and identified protocols issuing synthetic derivatives, offering insights on the optimal platforms for staking ETH. You can find more details in our article: Redefining Traditional Staking.

Subsequently, we transitioned from LSD to LSDfi, a move that enabled us to leverage Liquid Staking Tokens (LST) and enhance the yield of underlying assets. Our exploration extended to platforms such as Raft, Gravita, Lybra Finance, and Prisma Finance. Further details can be found in our article: A Comparative Overview of LST-backed Platforms.

Expanding from the overview of LSDfi, we delved into the entire LSDFi ecosystem. Our focus centered on UnshETH, Pendle, Flashstake, Eigen Layer, and LSDx. For a comprehensive understanding of the LSDFi landscape, refer to our article: Global Overview of the LSDFi Ecosystem.

To conclude our series, we presented a comprehensive overview of the LPDfi Ecosystem, elucidating how protocols can actively utilize Uniswap V3 LP positions as a foundation for building products. Our coverage extended to protocols such as Logarithm Finance, GammaSwap, Panoptic, InfinityPools, and others.

Given our deep involvement in liquid staking throughout the year, we strategically invested in protocols like Smilee Finance, Fluidity Money, Elixir Protocol, Restake Finance, and others. Each of these ventures demonstrated remarkable growth and gained substantial traction over time.

We strongly believe that the liquid staking ecosystem will continue to evolve, bringing forth more staking solutions and impressive yield rates.

2. LSDFi

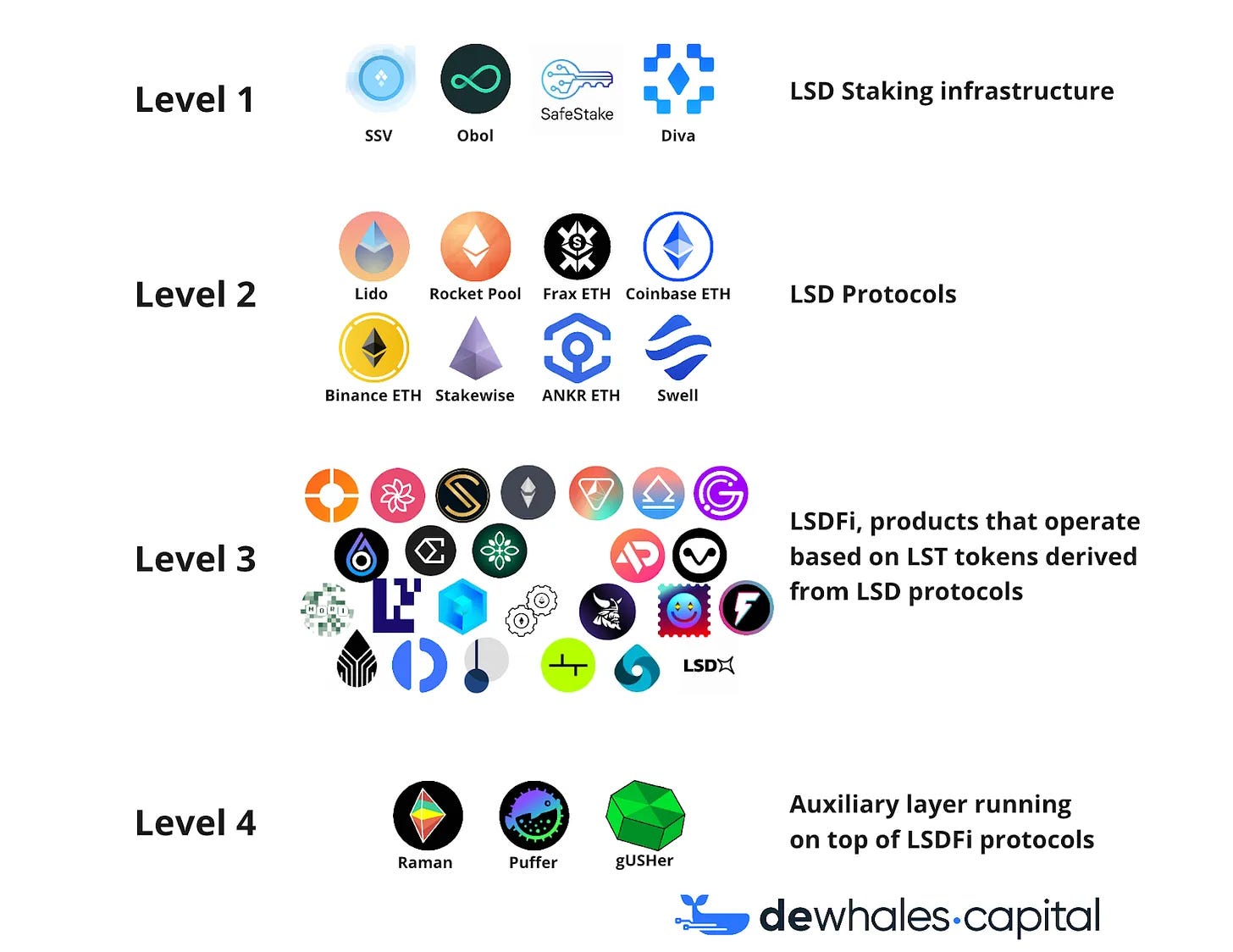

In 2023, it may seem that there were no major launches or upheavals. Indeed, the most significant event was the Ethereum Merge, which resulted in one of the longest and strongest trends of 2023. In other projects and protocols, the development of established technologies continued. Perhaps this year can be considered a year of accumulation not only for markets but also for technologies: the LSDFi scene was forming, L1 and L2 protocols were launched as new testnets and transitioned to mainnets—meaning, there was both parallel and sequential development based on existing technologies.

Therefore, the most notable trend was the development of LSDFi, as discussed in our series of articles (1, 2, 3), which saw a significant amount of innovation and projects over the year. Although this narrative is characteristic of most L1s with staking for validators and delegators (Polygon, Solana, Avalanche, Near, and others), it saw the most development in the Ethereum. However, it is worth noting separately that Near has recently been promoting the idea of restaking and LSDFi, and Solana has launched the new Token 2022 standard, which may open up a new phase of product development similar to Ethereum in the Solana.

Looking at LSDFi metrics, significant growth in liquidity is evident. Lybra Finance held the leading position for most of the year (over 50%), but its position shifted with the launch of Prisma Finance and Eigen Layer. Among LSD protocols, stETH Lido continues to hold the leading position.

The total value locked (TVL) in LSDFi increased to $1.69 billion, with eUSD from Lybra Finance dominating the market among LST-backed CDPs. However, as of November 2023, it yielded its position to a new player, mkUSD from Prisma Finance:

If we delve into the LSD landscape, we observe a consistent growth in the amount of staked ETH, and the market capitalization of the LSD market has reached approximately $27 billion, according to DefilLama data. Lido continues to maintain its leadership in this domain. When considering the overall volume of Ethereum staked (including direct staking), the numbers become even more impressive, reaching 28.75 million ETH ($64.1 billion).

Thus, overall, liquid staking currently stands as the largest sector within DeFi, boasting a market capitalization of approximately $30 billion, surpassing DEX and money markets. Of particular interest lately are the so-called LRT (Liquid Staking Tokens) - protocols designed for restaking. When Eigen Layer was initially launched, most users perceived it merely as a means to easily boost yields by staking their LST. However, at present, it serves as more than just a building block in LSDFi. Several projects are leveraging Eigen Layer for restaking to enhance their security, including AltLayer, Blockless, Celo, Drosera, Espresso, EigenDA, Hyperlane, Lagrange, Mantle, Polyhedra, WitnessChain.

In essence, LSDFi has come a long way from being just LST-backed CDP to evolving into a fully-fledged infrastructure layer. On top of this layer, foundational protocols are being developed, which may give rise to their distinct ecosystems and introduce new technologies and integrations. This significantly deviates from the paradigm observed in the comparison research between Curve and LSDFi: the farther a protocol is from its foundational layer, the less total value locked (TVL) and fully diluted valuation (FDV) it tends to attract. In this case, protocols built on top do not capture the value and users of the foundational protocol but have the potential to create their own value and user base.

3. Stress Testing Chain Resilience through Inscriptions

Towards the end of 2023, an event occurred that may be considered underrated - the introduction of Inscriptions. In essence, it represents a new approach allowing users to embed virtually any digital artifact directly into the blockchain, including images and text. Unlike traditional NFTs, typically stored off-chain and linked through metadata, these records are fully contained within the blockchain. While this trend initially began in the Bitcoin blockchain, it later transitioned to other chains. Due to the cost-effectiveness of descriptions, numerous ones can be created for the same unit cost.

Despite Inscriptions not being deemed a fundamental phenomenon, this event provided a robust test for the readiness of L1 and L2 chains to withstand genuinely significant and sustained loads. It also highlighted their vulnerabilities, primarily reflected in a sharp increase in gas costs, compounded by the simultaneous growth in the prices of the underlying tokens. The highest gas expenditure activity for Inscriptions occurred on the Avalanche C-chain:

If we exclude Avalanche from the analysis, we observe that the highest gas expenditure activity was also evident in Ethereum, Arbitrum One, zkSync Era, and BSC chains:

Moreover, when we look at the quantity of Inscriptions, it turns out that leading chains include Polygon, BSC, and Avalanche:

In the Arbitrum, an incident occurred where a failure occurred due to issues with the sequencer and channel amid the surge in chain traffic related to Inscriptions. As of December 15, Arbitrum One had generated 3.8 million Inscriptions, and by December 16, it reached 4.5 million. During the same period, gas usage amounted to $903,000 and $2.1 million, respectively. Two hours before the failure, Inscriptions constituted over 90% of the Arbitrum traffic. Before the outage, the number of transactions published per hour was approximately 10-20 times higher than the December average, leading to a halt in L1 batch publishing due to an inherent restriction on batches publishing speed. As a result, the Offchain Labs team, responsible for the Arbitrum sequencer, had to increase this limit, which, in turn, may carry risks of batches needing to be reposted due to transaction nonce issues.

In the Avalanche C-chain, gas costs surged nearly fourfold, and the cost of interacting with smart contracts (such as providing liquidity on Trader Joe) reached over 1 AVAX ($40+), which is quite close to Ethereum's gas prices. Interestingly, when looking at the Total Value Locked (TVL), there aren't as many active protocols in this chain compared to, for instance, Solana (with a total TVL of $988 million: $651 million - Benqi, $284 million - Aave, $130 million - Trader Joe, $64 million - GMX, and others below $50 million). This suggests a significant impact of Inscriptions on the activity of the Avalanche chain:

On the Ethereum chain, the cost of gas has increased about 6 times from a low point in October to a high point in mid-December and currently the swap price is hovering around $11-20. But in general, inscriptions are less active on the Ethereum chain than on other chains:

If we compare the cost of transactions in L2, there is also a disappointing dynamics: instead of a few cents, transactions now cost from 0.2 to 0.7$. And the record holders are Starknet and Polygon zkEVM, which contain STARK evidence in their technology - in them the price of transactions varies from 1.4 to 4$. And in theory, the transaction cost story could have a positive impact on Solana, which has recovered from the network outage. Plus, Solana has released a new token software, Token 2022, which allows you to create more customisable tokens with more mechanics and usecases than before. We wrote about this recently in our Solana Token-2022 Standard article. But in the case of Solana, it's also worth considering that interacting with DEX can be difficult lately due to the fact that transactions through Telegram bots are faster and transactions are often simply rejected.

But it's also worth bearing in mind that the Cancun-Deneb update is planned for January on the Ethereum, which aims to create "data blobs": a new transaction type intended to scale data availability for Layer 2 (L2) rollups. This consists of EIP-5656 and EIP-6780, which improve opcodes and optimise Ethereum's memory footprint, and EIP-4844, which aims to make transactions cheaper by reducing data size and block space with a new transaction type called "BLOB object migration". Aggregation sequencers (and possibly others) will use this new transaction type to publish data to the Ethereum chain cheaper than is currently possible. This could possibly change the landscape in the blockchain space again.

4. Bridgeless Future of 2024

In 2023, we published two articles dedicated to bridges. The first article delved into the infrastructure of blockchain bridges, exploring their types, associated risks, and providing a brief overview of cross-chain communications.

The second article conducted a thorough comparison among LayerZero, Chainlink CCIP, and Cosmos IBC. It highlighted the similarities between LayerZero and Chainlink, while also examining the Hub & Zone Infrastructure of Cosmos.

With the continuous evolution of Layer 1 and Layer 2 blockchains in the space, liquidity is becoming increasingly fragmented across various chains. As the crypto industry has witnessed substantial growth, and we anticipate further expansion in 2024, a surge in liquidity is expected. This is where bridgeless systems may emerge as a fundamental component for seamlessly transferring value among different chains.

5. Intertwining RWAs, Blockchain and Web3 Markets

Just in the vertical of RWAs alone, we have seen multiple protocols jump at the opportunity of onboarding assets from the traditional markets, be it forex trading, equities or bonds. This was evidently true from the discussions around US treasury bills coming on-chain, with Web3 protocols turning their attention to regulated brokers and intermediaries that are able to facilitate purchases with on-chain liquidity through stablecoins such as USDC.

However, as the ever-changing sentiment of Web3 dictates, risk-free returns via treasuries with a macro outlook prediction for rate cuts will determine if this liquidity is sticky, especially with the lessened friction of moving funds with the use of blockchain technology. One of the bigger questions these protocols who invested heavily in building traditional bridges should start asking is, can they keep up with the Web3 competition?

5.1 Perspective 1: Web3 Markets’ Adoption of RWAs

2023 was the year of US treasury bills onboarding to Web3 protocols, as holders of stablecoins flocked to get a piece of relatively high risk-free interest rates. This movement was also driven by lower yields seen across DeFi protocols where there was diminished risk to reward on stablecoin farms and liquidity pools. Moreover, some of these protocols were offering tokenised bond offerings on top of treasury bond yields, enabling global users accessibility to US-based products while diversifying their on-chain portfolio. In addition, we observed multiple protocols that were venturing into small/medium enterprise financing, luxury goods, digital identities on Web2 and infrastructure to help bring assets on-chain.

Some notable investments made by Dewhales Capital within this space include Blueberry Finance - (T-Bills).

This sector overall is still experimenting with the asset classes that might bring value to on-chain users, with the majority continuing to focus on financial instruments from the traditional finance space. It is also apparent from the direction that some blockchain foundations have made in terms of looking into permissioned zones on their blockchains/protocols (e.g. Injective for financial institutions, KYC requirements for US-based investment instruments) may point to a potential uptick in digital identities on-chain for whitelisting purposes. With the adoption of such instruments from users, more protocols in the lending and trading space are also looking to onboard these receipts as high-quality collateral, which may introduce more trading pairs that are interest-bearing in nature (e.g. sFRAX/wstETH) and more efficient looping strategies for yield boosts.

On that note on digital identities, we expect to see more protocols blend in pseudonymity of on-chain users with verifiable credentials that grant access to specific features and investment types due to evolving regulations and there could be opportunities presented to further develop necessary infrastructure.

5.2 Perspective 2: RWAs’ Adoption of Public Blockchains

One interesting sector that has yet to unfold within the RWA space would be Green Financing and ESG-related reporting. An example of this includes Hedera Guardian being provided as an SDK for companies to begin their carbon footprints on-chain, providing them standardised templates for reporting and accounting their activities depending on their jurisdictions. If we were to take a look at how their ecosystem has been developing, we see companies such as ServiceNow (American software company providing workflow management platforms) and Standard Bank (South African bank and financial services group) delving into the usage of Hedera Guardian for themselves and for their clients potentially.

LandX, which was launched recently, also provided new ways for agricultural farmers to obtain financing through blockchain, while investors could use this as a way to hedge against inflation through the underlying ownership of farmland and crops of choice. It is also an example of how real world production, data validation and more transparent financing opportunities have crossed paths via blockchain, to which many RWA problem statements begin from.

Lastly, we continue to expect growth driven from traditional finance being tokenised on-chain, with the likes of JP Morgan and Citi looking to adopt Avalanche as the blockchain of choice to expand their service offerings to on-chain clientele, with more to follow suit. This will probably be driven via a permissioned blockchain route, but it is also one of the ways public blockchain adoption will continue to increase over time as enterprises find the correct balance between regulation, data privacy and liquidity risks.

5.3 Perspective 3: Investor Interest and Liquidity

With the macro environment seemingly indicating a much more risk-on market going into 2024, and with expectations of interest rates getting cut in the near future, protocols that have focused on obtaining liquidity via treasury bills and bonds are probably going to face strong liquidity outflows as investors seek higher returns. This is also true as yields make a comeback across DeFi farms and incentive programmes come to life as we have seen with the recent rounds of Arbitrum incentivisation. However, it also provides an interesting tipping point for RWA-based lending, be it traditional company bonds or stablecoin lending to hedge funds in exchange for market making revenue as volatility is usually ever present in risk-on markets. Moreover, investors might be keen to invest into leveraged ETFs and commodities via on-chain in search for multiplied returns, which would also bring volume back to trading protocols.

However, we might be seeing liquidity inflows from different interested parties, such as DAO treasuries, that seek returns with minimal risk while focusing their efforts on launching new products and services to users within a risk-on environment. This might counter some of the liquidity outflows as mentioned above. Also, considering that treasuries are typically of much larger sizing, they have to seek avenues that can sustain yield at large sums. These considerations, coupled with a growth in potential lending markets focused on financing activities, could continue to fuel the growth of products such as sDAI from MakerDAO and sFRAX from Frax Finance, as well as partners such as Centrifuge.

6. Looking Forward To 2024 For RWAs

Increased uptake in RWA loans and private equity (e.g. real estate, credit notes) to back stablecoin yields:

Onboarding real world loans to finance companies and their respective activities

Lending for market making activities

Tokenised real estate rental yield

Tokenised hard assets (e.g. precious metals) as lending collateral

Expansion of NFT usage around traditional assets to grow NFT-Fi usage and liquidity rehypothecation

Continued maturation in ESG financing and carbon trading alongside global macro trends on sustainability

Increased trading volume on-chain around commodities and onboarding of ETFs on the back of potential Bitcoin and Ether ETFs:

Increased volatility encouraging trading positions in traditional assets

Opportunities for offering levered ETFs for trading on-chain

Growth of options protocols and respective trading strategy implementations

Increased revenue sharing opportunities for trading protocols

Increased support for yield-bearing positions with traditional finance instruments and commodities as collateral:

Enablement of traditional assets represented as digitised collateral to enhance liquidity efficiency for traditional asset holders

Allowing leveraged borrowing/lending to keep yield desirable in a risk-on environment

Layer 1 blockchains supporting permissioned use cases for regulated entities:

Increased interest in offering tokenised versions of products on-chain but in a regulated, permissioned manner

Diversification of stablecoins that are non-USD based (which could lead to renewed interest in on-chain forex trading)

Potential comeback for metaverse narratives in relation to traditional enterprise service offerings

Utilisation of yield-bearing tokens as trading pair bases against other yield-bearing volatile assets:

Continued growth in products and services that are based on interest rate spreads

New delta/gamma-neutral structured products as vaults using interest-bearing tokens

New arbitrage opportunities for mispricing between interest-bearing tokens cross-chain

Conclusion

But at the same time, if we compare it to 2021 and 2022, 2023 probably left a calmer impression, without high-profile technology launches and scandals that shook the whole industry. Even in the case of high-profile investigations and scandals: it was mostly all a continuation of what happened in 2021-2022. But the most important observation is probably that the crypto industry is living at its own pace, not deflating and continuing to grow, despite the complex geopolitical environment around the world, with successive crises and monetary tightening by Western central banks in an attempt to curb inflation, the prolonged kinetic conflict in Europe and a new one in the Middle East, and the long-term effects of the Covid-19 pandemic.

Also 2023 has shown that L2 and L1 in their current form can and should still be optimised further, as the idea with vertical scaling via subnets in Cosmos, Avalanche and Polkadot are not in high demand at the moment compared to the various L2s that are entering an increasingly active phase of competition for users and liquidity. Plus, technically, subnets are directly competing with horizontal scaling in the form of L3s, which also have the narrative of separate block spaces for dApps.