Curvance Explained: A Modular Multi-chain Money Market

An overview of how such a simple idea as money market aggregation actually works, even with a modular structure with a breakdown of strategies

Disclaimer: The content presented in this article, along with others, is based on opinions developed by the analysts at Dewhales and does not constitute sponsored content. At Dewhales, we firmly adhere to a transparency-first philosophy, making our wallets openly available to the public through our website or DeBank, and our articles serve as vehicles for self-expression, education, and contribution to the ecosystem.

Dewhales Capital does not provide investment advisory services to the public. Any information should not be taken as investment, accounting, tax or legal advice or as a recommendation to purchase, sell or hold or to pursue any investment style or strategy. The accuracy and appropriateness of the information is not guaranteed by Dewhales Capital.

Introduction

1. Curvance architecture

2. Curvance flow

3. Curvance dApp overview

4. Tokenomics and Metrics

5. Backers

7. Introducing ZKX - Built on Starknet

8. Product overview

9. Tokenomics

10. Backers

11. Conclusion

Introduction

In the past 2 years, the direction of development of Fat-protocols in the crypto industry, focused on end-users and working on UI/UX to make it easier and more intuitive for users to interact with the crypto world, has become increasingly evident. This means that the industry is moving away from the paradigm that Fat-protocols are simply blockchains at the foundational level. Additionally, there are now many different networks emerging.

Therefore, it seems that there is a gradual shift towards web2, where protocols built on top of blockchains begin to provide functionality and user experience that attract more attention, resources, and liquidity to the protocols themselves. Just like a person using health-app metrics doesn't need to know about TCP/IP, HTTPS, and other backend things, but desires a functional application with an understandable interface.

Similar concepts are currently observable in the crypto industry. Now we can swap directly within wallet extensions or transfer between chains within a DEX application. The ability to swap multiple assets at once has ceased to be exotic, despite being a basic function from a user experience perspective, but it was a technical innovation. And perhaps, along with this, the approach to cross-chain compatibility and unified liquidity is changing: from low-level native solutions like IBC Cosmos, which were supposed to become a unified liquidity hub, to high-level solutions that operate on top of cross-chain protocols such as Wormhole, LayerZero, and Axelar.

Curvance is precisely representative of this trend. It is a modular multi-chain money market for yield-generating assets and any other ERC-20 tokens. Initially launched on Ethereum, Arbitrum, Blast, Base, Optimism, and Polygon zkEVM, it aims to establish itself as the de facto money market for any ERC-20 token. It operates on the principle of isolated lendings, which allow leveraging for LPs and LSDs. What does this mean? Let's delve into Curvance and understand how it works.

1. Curvance architecture

The initial idea was very simple - it was just a lending and borrowing market for Curve and Convex. But then it evolved into something much larger due to support for more networks and protocols. It is the architecture of Curvance that gives it modularity and the ability to support different protocols. It can be classified as a Fat-dapp, which combines multiple blockchains and protocols, and aims to become the top layer above lending and income-generating applications. Curvance seeks to unlock the potential of yield-generating tokens like cvxCRV, auraBAL, & LP tokens by allowing users to earn original platform APR while using deposits as collateral for stablecoin loans.

At its core, Curvance consists of four main components:

Protocol Architecture: Utilizing the ERC-4626 standard, Curvance provides a plug-and-play solution for any ERC-20 token. The ERC-4626 storage is a key component of Curvance's modularity, allowing for isolated storages that operate independently of each other. This standard also facilitates the automatic accrual of collateral loans, maximizing profitability for those with active loans. Additionally, third-party developers will have the opportunity to create complementary solutions within the Curvance ecosystem.

Money Market: This is the heart of Curvance, regulating collateral mechanisms, Health Factor, interest rates, and collateralization. Curvance's contracts are based on established lending protocols like Aave and Compound, using a hybrid approach between the shared pool model and the isolated pool model.

Multi-chain Architecture: Support for multiple chains is implemented through Wormhole. This component manages not only cross-chain liquidity pools but also the Multi-chain Gauge, which incentivizes liquidity across all supported chains and allows users to vote for any pool regardless of where liquidity is locked. Users do not need to pay gas fees for voting thanks to the decentralized Snapshot system. Besides direct users, this infrastructure component of Curvance can be utilized by other protocols and blockchain networks, enabling user stimulation through airdrops, STIPs, and grants. This facilitates the implementation of complex targeting mechanisms and the stimulation of desired user bases with liquidity incentive programs.

Dual Oracle: To maintain market stability, Curvance will utilize a dual oracle model. The oracles used may vary, including Chainlink, Curve, UniV3, API3, Redstone, and more. This means that Curvance can support any asset using almost any channel, including off-chain and on-chain Oracle solutions. In case of price discrepancies between oracles, asset borrowing is automatically suspended to prevent, for example, flash loan attacks. The protocol will use the most advantageous price variant to protect lenders.

Furthermore, Curvance distributes protocol fees in stablecoins, and therefore, integrating CCTP into Wormhole allows for better scalability in terms of fee distribution. CCTP is an inter-chain transfer protocol from Circle, ensuring secure USDC transfers between blockchains through built-in burning and minting. Moreover, enabling Native-USDC transfers using CCTP requires just 3 lines of code for Wormhole Connect, significantly simplifying infrastructure and reducing risks. Additionally, Curvance collaborates directly with Wormhole on creating open-source multi-chain solutions developed by Curvance.

Another crucial aspect is a focus on enhancing UI/UX. The Curvance team emphasizes that the protocol is initially complex for those not familiar with crypto and DeFi mechanics. Therefore, the initial target audience consists of experienced DeFi users. However, there is a vision that over time, the Curvance team or someone else may create interface applications where understanding the intricacies of the process is unnecessary, requiring only a few mouse clicks to deposit tokens and take out loans against anything. In the future, the team plans to introduce 2 versions of the interface: one for advanced users and a more simplified one for those who don't need a detailed interface.

2. Curvance flow

If we were to outline the Curvance Flow in broad strokes, it seems quite simple:

However, thanks to its comprehensive architecture, which integrates not only protocols but also different networks, with Curvance, users are not limited to the traditional choice between capital efficiency in money markets and other aspects of DeFi. This allows users to employ flexible and multi-faceted strategies, such as depositing ETH in Aave to obtain leverage. So, in reality, it's a bit more complex.

It's also worth noting that depending on the asset, the Loan-to-Value (LTV) ratio may vary, determining the amount of stablecoins users can borrow against their asset, and the borrowing capacity may depend on the utilization of a specific pool. In addition to the dual oracle, Curvance has an interesting liquidation model - the "Dynamic Liquidation Engine," which operates similarly to DCA strategy (when a trader averages their position by buying or selling in parts). This allows borrowers to feel more confident in the face of strong market movements without instantly losing their entire position.

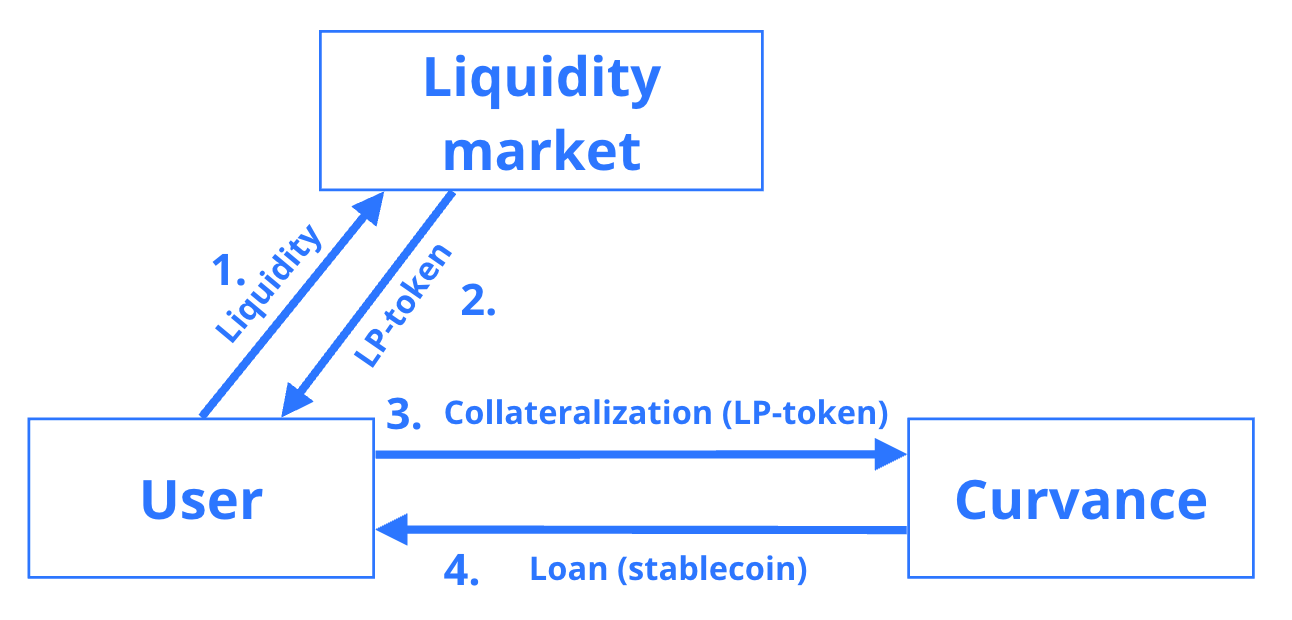

So, how does this work for users when they simply want to get a loan/credit:

Suppose a user has LP tokens like auraBAL or cvxCRV wrapper tokens.

The user visits Curvance and simply takes out a loan against their auraBAL or cvxCRV collateral. Upon collateral deposit, the user receives c-auraBAL or c-cvxCRV tokens, and the collateral token is assigned to the corresponding pool.

The c-auraBAL or c-cvxCRV tokens can be used to borrow stablecoins from lenders, with the user paying interest for it.

Meanwhile, in Curvance, other processes are underway: for instance, if a user (borrower) collateralizes cvxCRV, Curvance sends it to the original Convex pool to start generating yield for Curvance itself.

Alternatively, there could be a slightly more intricate scenario, where a user has a more complex strategy:

The user wants to acquire more assets and deposit them into credit pools, such as GLP.

The user deposits GLP into Curvance.

Curvance redirects the provided GLP back into the base protocol to earn yield (GMX) while simultaneously allowing the user to take out a loan against it.

The user receives so-called cTokens, representing their collateral, which can then be used to repay the collateral provided once the loan is repaid.

The user again utilizes the stablecoins from GLP obtained in exchange for cTokens.

For protocols, the Curvance works as follows:

Suppose Aura Finance wants to increase rewards for its auraBAL pool (a liquid wrapper token users receive for providing liquidity in an 80BAL20ETH pool on Balancer).

Aura purchases veCVE tokens and votes to increase the pool.

With increased liquidity and TVL accordingly, rewards in CVE rise, further incentivizing users to provide liquidity to the auraBAL pool, creating a loop: more liquidity → more TVL → sensors generate more emissions → even more users see attractive yields.

VeCVE holders can additionally vote for auraBAL sensors and receive kickbacks from Aura, further enhancing the pool's attractiveness.

Curvance will also support Pendle LP as collateral, long-term loans from Alchemix and alUSD. Furthermore, users will even be able to collateralize RWA through TangibleDAO! They tokenize real-world assets such as real estate, art, wine, watches, gold, etc., which serve as collateral for the rebase stablecoin USDR. USDR can then be provided in LP on Velodrome or AerodromeFi and use these LP tokens as collateral on Curvance.

For example, Convergence plans to aggregate and accumulate CVE tokens, allowing users to access cvgCVE and stake without locking. You can learn more about how Convergence works and its potential impact on CVE through its mechanics in our separate article about Convergence.

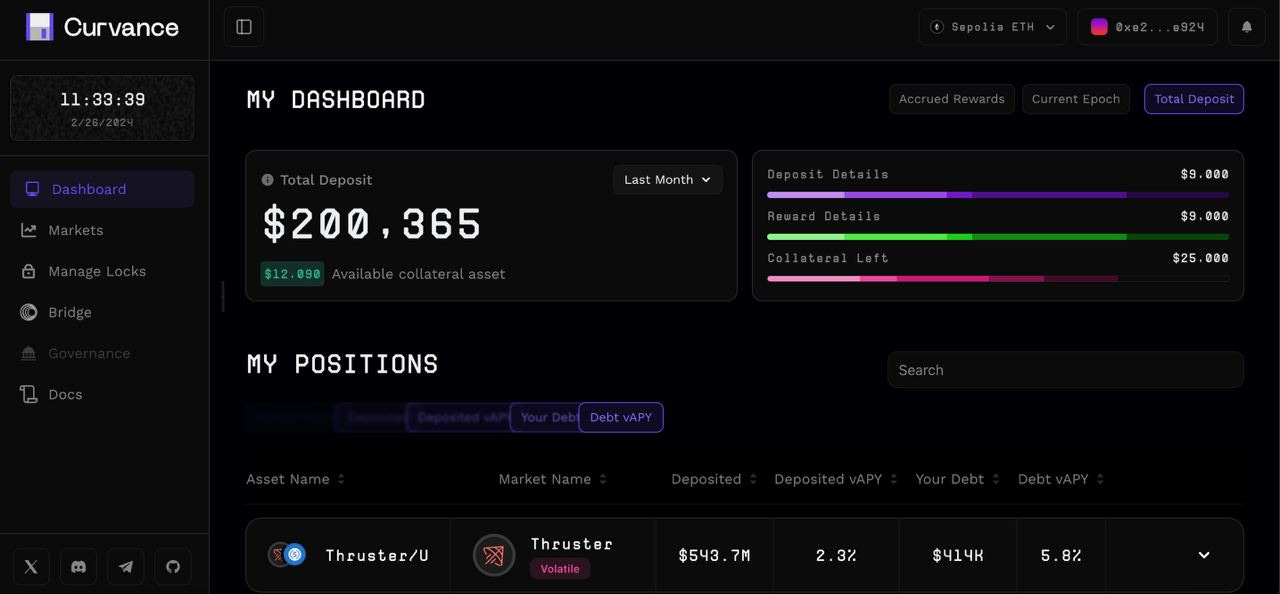

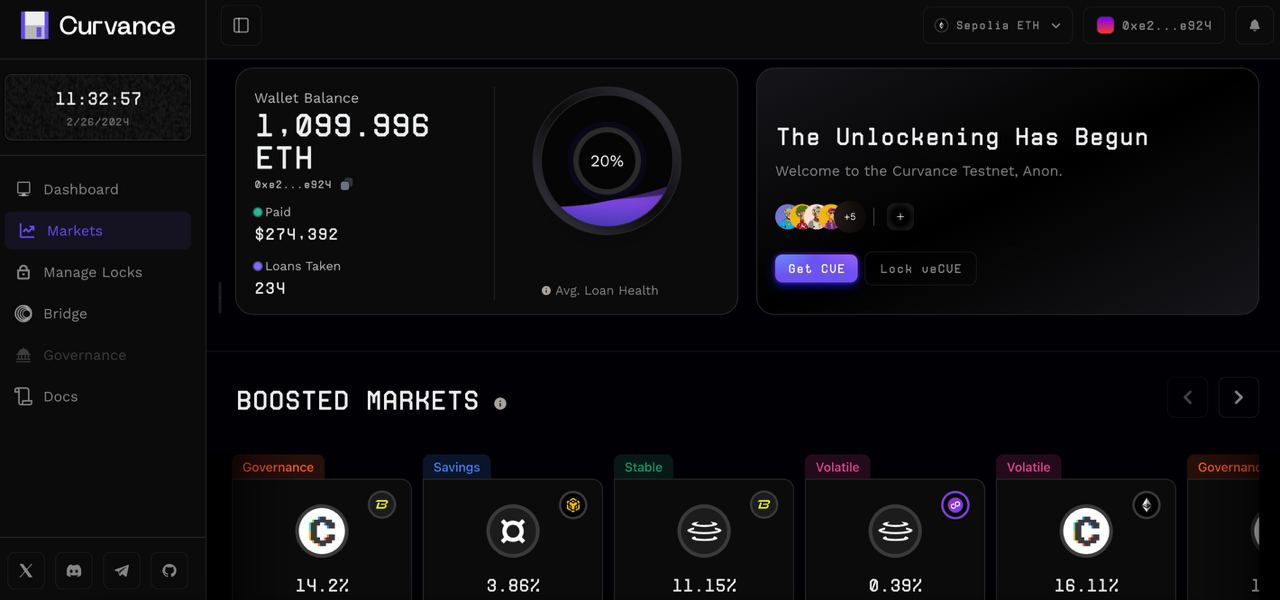

3. Curvance dApp overview

At the moment, the Curvance dApp has not yet launched, but we can envision how it will look based on their description of the workflow. Firstly, users will be able to switch between various assets and LPs with just one click directly within the interface, eliminating the need to access different dApps and switch between multiple tabs. Secondly, Curvance will automatically allocate users' deposits to the appropriate platforms, further simplifying interactions. And thirdly, users will be able to use any asset in Curvance’s Zapper to exchange it for LP and other assets. This all seamlessly fits into the philosophy of a Fat protocol, which allows for aggregation not only of different protocols and assets but also of user bases.

4. Tokenomics and Metrics

The primary native token of Curvance is CVE. Its mechanics, in broad strokes, are similar to those applied in CRV and CVX. CVE holders can lock them into veCVE and participate in the DAO's governance. Additionally, veCVE can be locked to boost voting power, vote for emissions distribution in credit markets, and receive a share of platform fees. veCVE can be locked either permanently, with the option to enable or disable at any time, or relocked every few weeks.

Total CVE supply: 420m

59.25% [248,850,040.88] Gauge Emissions - released continuously over 15+ years with distributions based on biweekly gauge weights.

3.75% [15,750,002.59] Community Incentive Program

2% [8,400,001.38] Initial Pool Liquidity - 100% of funds from the LBP will be used for DAO controlled, protocol owned liquidity.

13.5% [56,700,008.32] Team - Unlocked monthly over 4 years and 25% will be vote-locked on TGE in the CVE locker.

6% [25,200,004.14] Seed Raise - Vote-locked on TGE in the CVE locker and vested for 1 year.

1% [4,200,000,69] Early Backers Raise - Vote-locked on TGE in the CVE locker and vested for 1 year.

14.5% [60,900,010] Treasury - 25% will be vote-locked on TGE in the CVE locker.

5. Backers

Among the Backers who committed $3.6m, notable organizations include: Dewhales Capital, Homeless Ventures, Redacted Cartel, Alchemix, Castle Capital, Midcurve, 369 Capital, Spiral DAO, Millennium Club, Tailored, BotBlockDAO, as well as Andy, Mr. Block, Grills, Small Cap Scientist, CoinFlip Canada, and others. Additionally, Curvance has received grants from the Wormhole Foundation, Arbitrum Foundation, and Lybra to create a unified liquidity layer in DeFi.

Among Curvance's current partners/integrators are protocols such as Convex, Convergence Finance, Pendle Finance, Redacted Cartel, TangibleDAO, Prisma Finance, Lybra Finance, Balancer, Camelot, Velodrome, Frax, Stader, Swell, Aura Finance, Alchemix, Swell Network, and others.

Conclusion

Curvance is being developed with a meticulous approach, evidenced by both the volume of code (over 15k SLOC), which has been audited by Cantina with public audit competition with $375k reward pool and is awaiting at least 3 public audits. Other security partners include Trust Security (Top C4 Whitehat) and Y-Audit (Yearn Audit) to conduct internal review and Trail of Bits to conduct stateful fuzzing suite on Curvance’s codebase. Curvance is also moving very intensely towards partnerships and intgerations, increasing their number. During the final product polishing stage, Curvance continuously revolves in the DeFi space, connecting numerous protocols and elements, thus laying a solid foundation for various mechanics and collateral assets. Users will be able to collateralize not only LP tokens from regular liquidity pools but even indirectly - real-world assets!

On one hand, it may seem straightforward to simply aggregate all protocols that provide LP tokens and LSD to their users. However, within DeFi lies a vast array of complex mechanics, and Curvance elegantly wraps them up. It's precisely how they unfold the meaning of integrations, narrating the entire strategy path from start to finish, that allows users to form a vivid and comprehensible picture of a complex strategy from inception to completion.

The contribution to popularizing complex DeFi strategies cannot be overstated, as Curvance lays the groundwork for a platform that may, in the future, enable non-DeFi professionals to obtain loans or provide liquidity for lending in just a few clicks. Meanwhile, under the hood, intricate mechanisms akin to sophisticated clockwork with numerous gears will be at work. Just as when you buy expensive, intricate timepieces, marvels of engineering, you don't need to understand the arrangement of every gear, how they rotate in relation to each other, or how the hands move differently. You simply glance at the dial and occasionally wind the watch or change the battery.

Curvance links:

Website | Twitter | Discord | TG Community | Documentation