LPDFi: The Future of Liquidity Handling

What is LPDFi, how it works and an overview of projects in this direction: Logarithm, Orange, GammaSwap, Panoptic, Dopex, InfinityPools and Limitless.

Disclaimer: The content presented in this article, along with others, is based on opinions developed by the analysts at Dewhales and does not constitute sponsored content. At Dewhales, we firmly adhere to a transparency-first philosophy, making our wallets openly available to the public through our website or DeBank, and our articles serve as vehicles for self-expression, education, and contribution to the ecosystem.

Dewhales Capital does not provide investment advisory services to the public. Any information should not be taken as investment, accounting, tax or legal advice or as a recommendation to purchase, sell or hold or to pursue any investment style or strategy. The accuracy and appropriateness of the information is not guaranteed by Dewhales Capital.

Introduction

1. The Chain of Derivatives

2. How LPDFi works

- Logarithm Finance

- Orange Finance

- GammaSwap

- Panoptic

- Dopex

- InfinityPools

- Limitless Finance

3. Market Impact

Conclusion

Introduction

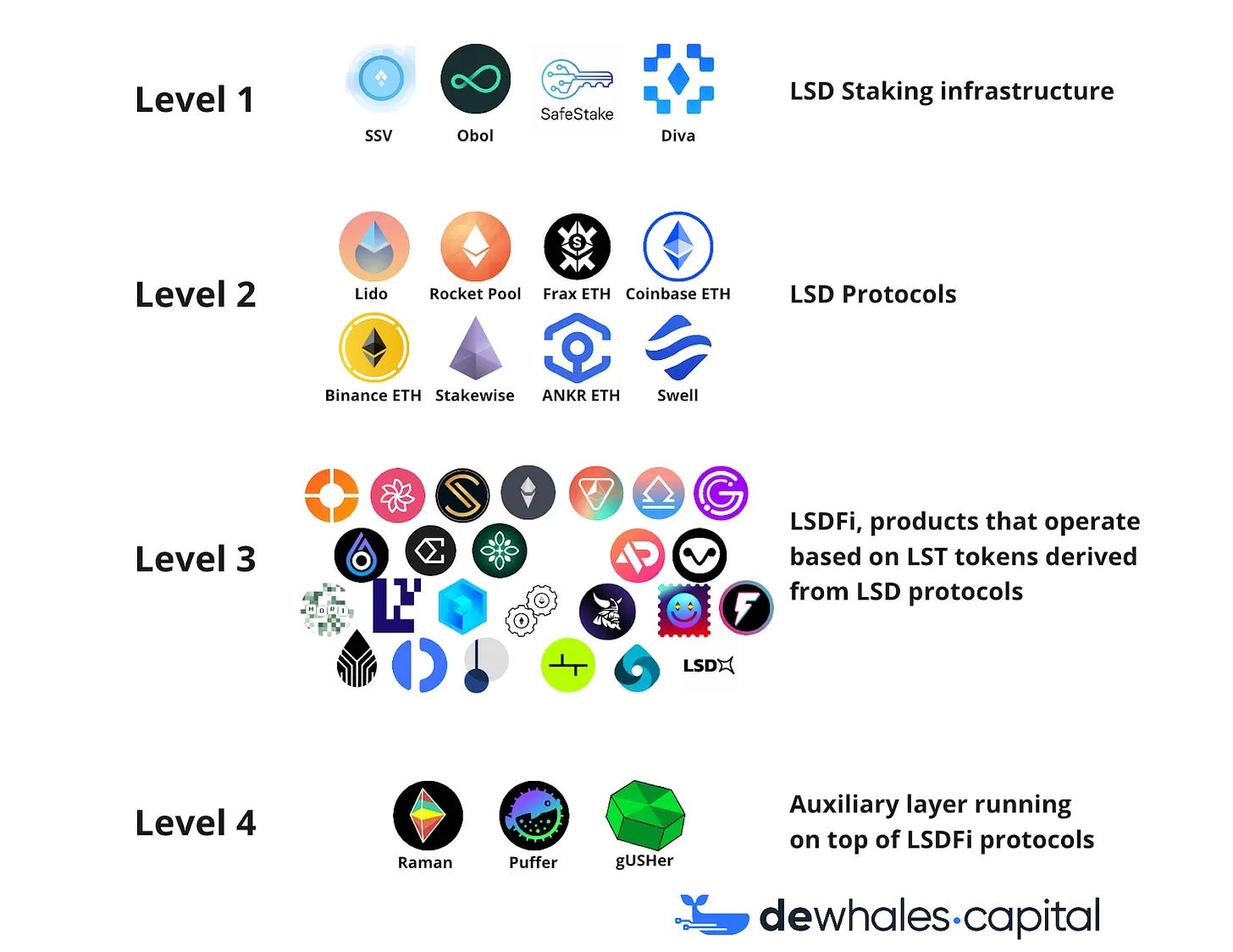

In 2023, we're exploring various narratives such as SocialFi, with friend.tech being the most popular representative; zk rollups, including Scroll, zkSync, and Starknet entering the space (check out our series of articles about zk rollups); Real World Assets with projects like Maple Finance and Goldfinch; and, of course, Liquid Staking Derivatives protocols like Raft, Gravita, Lybra, Eigen Layer, and others.

However, the liquid staking field has been progressing so rapidly that a new narrative is emerging, known as LPDFi (Liquid Providing Derivatives Finance). In this article, we'll delve into a thorough explanation of this new narrative, highlighting the main protocols pioneering the space. But be warned that it's likely that LPDFi doesn't work the way you might imagine from the LSDFi analogy. Well, let's dive deeper into it.

1. The Chain of Derivatives

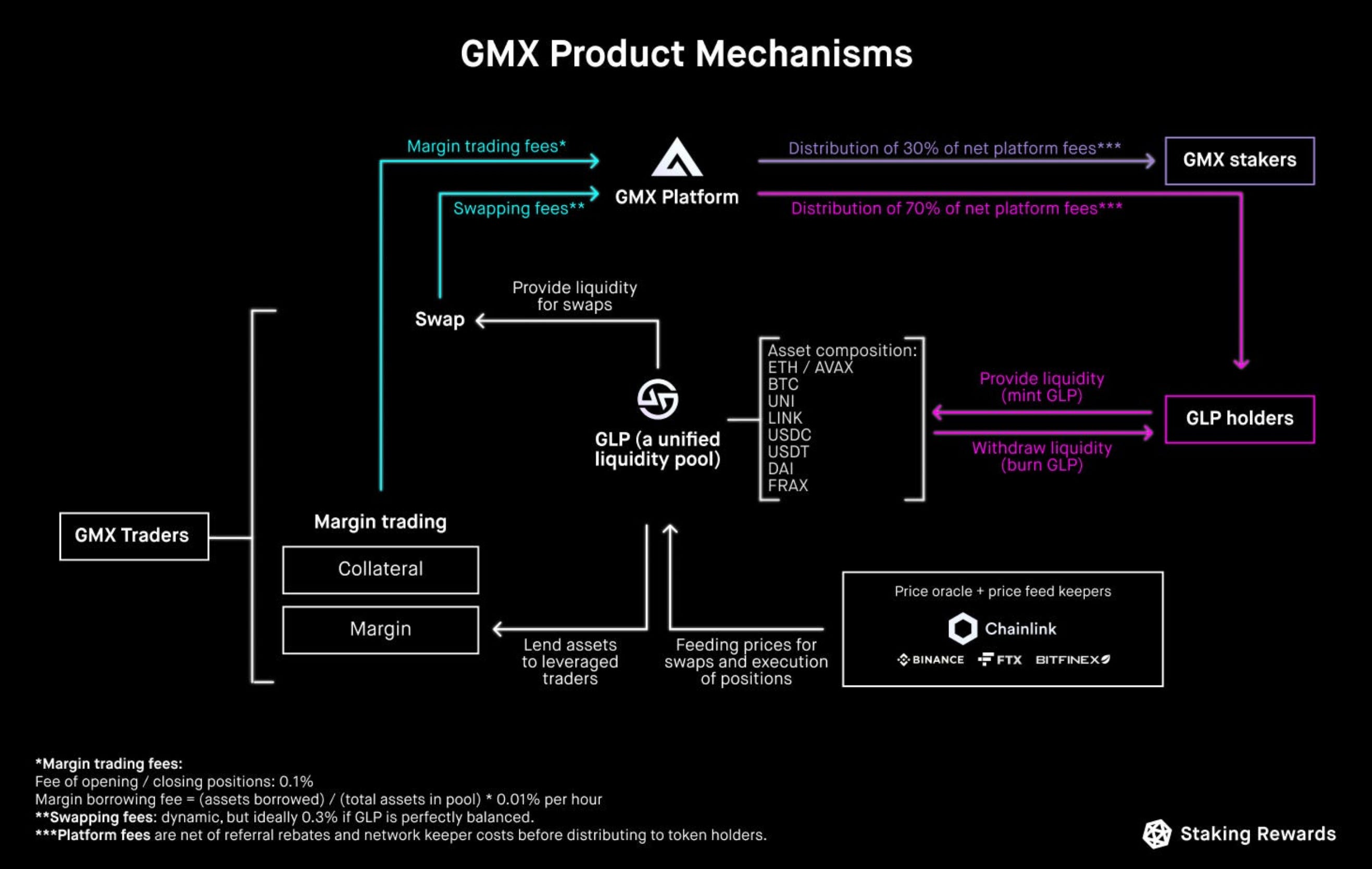

First of all, it’s important to understand the evolution of the derivatives market in crypto. One of the first protocols leading the derivatives market was GMX, which allowed the users to trade crypto derivatives directly from their wallet (on-chain) with up to 50x leverage, similarly to how it's done on a centralized exchange. The token holders could stake GMX to get additional rewards. However, the key problem that was spotted there is that staked tokens become illiquid.

This enabled the creation of the new narrative called Liquid Staking. One of the first protocol pioneering in Liquid Staking became Lido Finance. Lido provides users with tokenized representations of staked assets at a 1:1 ratio. This grants them liquidity for their staked PoS tokens, enabling them to earn staking rewards through Lido while engaging in other on-chain DeFi activities to gain extra yields, such as collateral for lending and yield farming to maximize rewards.

Lido and other LSD-protocols are enabled users to stake even a fraction of 1 ETH to accumulate block rewards. Upon staking their ETH, users receive stETH (rETH, swETH, sfrxETH and others) an ERC-20 token representing their deposited ETH at a 1:1 ratio. The stETH and other LST tokens are generated upon depositing funds into the LSD-protocols staking pool smart contracts and will be removed (burned) when users withdraw their ETH tokens (if you want to learn more about liquid staking, check out our article where we dive deep into liquid staking derivatives). And the use of LSD protocols is only growing.

The next step in liquid evolution was LSDFi, which allowed us to utilize LSD and optimize the yield of underlying assets. The rapid evolution of LSDFi gained momentum during the months of March and April 2023. This emerging trend involved leveraging ETH derivatives for yield management and recollateralization through various protocols such as ACID, AURA, FXS, Raft, LSDx, 0xACID, Agility AGI, unshETH, Lybra, and others.

And now during constant evolution we have a new narrative – LPDFi which stands for Liquid Providing Derivatives Finance. Similar to how LSDFi optimizes the potential of LSDs, LPDFi maximizes the capabilities of LPDs. That said, LPDFi is not just about providing liquidity tokens or stablecoins in exchange for underlying tokens as collateral or staking. In fact, it would be quite difficult for an untrained person to understand what LPDFi is from the Liquid Providing Derivatives side despite the large amount of material on the topic. Let's try to understand what it is further with the use of illustrative examples in the form of brief project reviews.

Let’s dive deeper into the LPDFi narrative and find out what it brings to the table.

2. How LPDFi works

In the previous section, we said that LPDFi benefits from LPD in a similar way as LSDFi benefits from LSD. But what are the LPDs? Liquidity Providing Derivatives are the protocols actively using Uniswap V3 LP positions to build products on top of it. LP tokens that Liquidity Providers get from providing liquidity act as yield-generating assets. This process enables creating new protocols like options, perpetuals, lending platforms, and others, we’ll explore them more in the next section.

Advantages provided by LPDFi:

For users: Increased profitability from liquidity farming through additional incentives in project tokens + LPDFi yield and reduced IL (LPDFi projects primarily focus on IL risk hedging). Additionally, LPDFi simplifies the provision of centralized liquidity for new users, eliminating the need for regular LP position calculations and adjustments to optimize yield.

For Uniswap v3: Increased liquidity, user base, and transaction volume.

LPDFi projects primarily utilize Options to mitigate impermanent losses and streamline LP operations in Concentrated Liquidity AMM (CLAMM), or, in other words, make more efficient use of liquidity.

Another feature common to LPDFi protocols is the absence of oracles in the protocol operation architecture.

However, the main problem Liquidity Providers currently face is Impermanent Loss as current hedging techniques aren't maximizing Uniswap V3's potential. To solve this problem, the first LPDFi Protocol was created which is called Logarithm Finance.

This protocol has 2 main functions:

Route liquidity through various LPDs to achieve highest returns

Hedge exposure to volatile assets to escape Impermanent Loss

Logarithm Finance

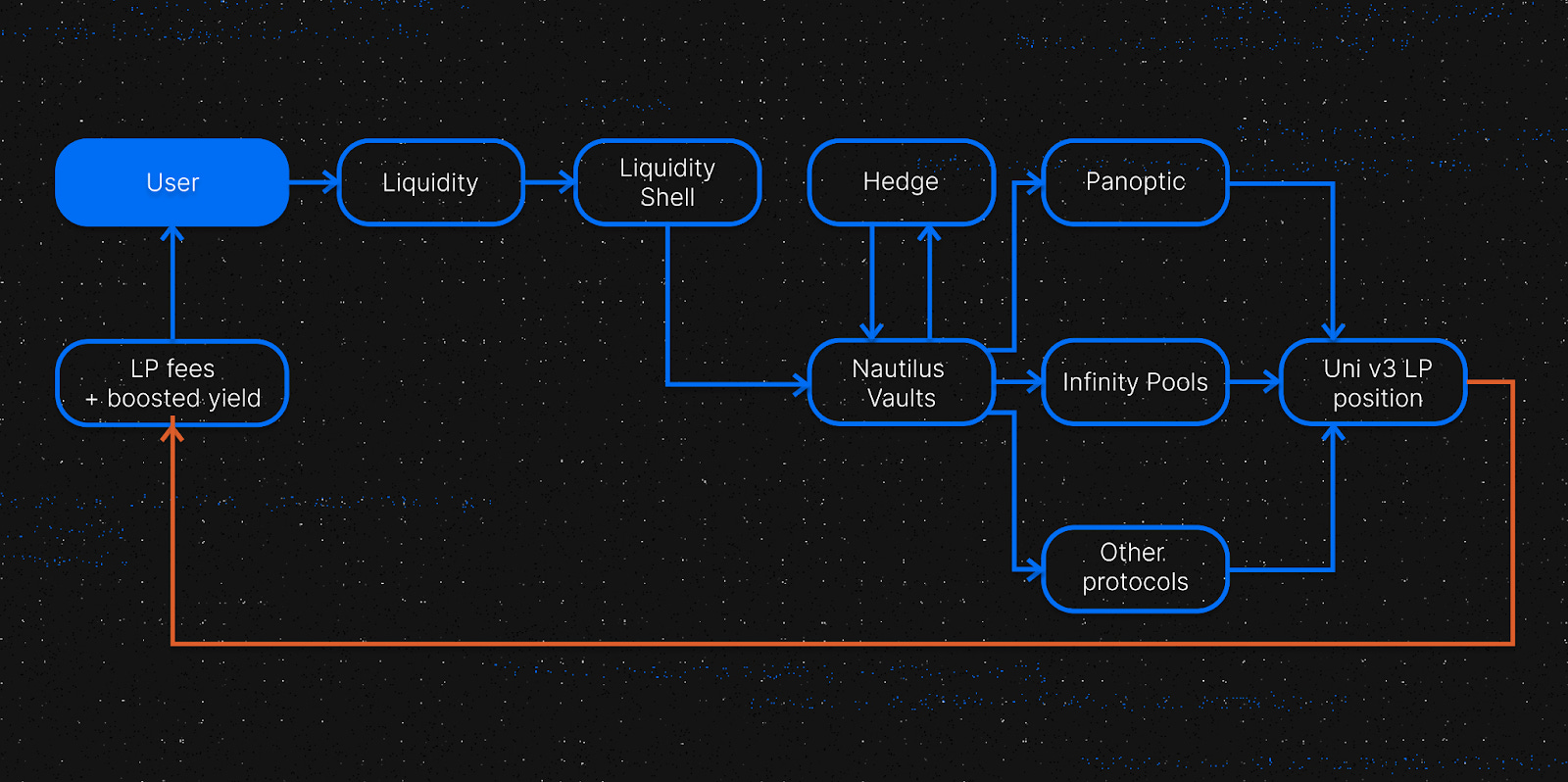

For routing liquidity, Logarithm came up with a mechanism called Liquidity Shell. It routes users’ deposits to the highest-yielding strategies across LPDs. To maximize efficiency, users are able to deposit single-sided liquidity, as well as decide if they want to use the Nautilus Vault strategy. Nautilus Vault hedges their position in a delta-neutral way using GMX perpetuals as a hedging vehicle.

Additionally, Liquidity Shell enhances capital efficiency and mitigates impermanent loss risks, making liquidity provision more appealing. Moreover, it directs more liquidity to LPD protocols like Panoptic and Smilee, amplifying their visibility and attracting additional users.

To hedge exposure to volatile assets and minimize the risk of impermanent loss, Logarithm uses their own Nautilus Vault. When you deposit the assets, the protocol opens an active highest volume LP position on Uniswap V3 with a narrow range and simultaneously hedges the volatile asset using decentralized derivative exchanges. By using Nautilus Vault, Logarithm is able to balance liquidity provision and risk linking Uniswap V3 and GMX. Here’s the overview of how Nautilus works:

Users deposit assets, and the vault optimizes allocation between liquidity and hedging

It creates a concentrated liquidity position while hedging with a short GMX position, ensuring balance and predictable returns

The vault adapts to maintain balance and modifies base liquidity ranges according to spot price

Backtests influence base range, trigger range, and re-hedging thresholds based on market volatility

The vault tracks fees and borrowing rates, auto-adjusting positions if market conditions change

So, Logarithm Finance acts as a Liquidity Layer for LPD protocol pioneering LPDFi space, now let’s explore what LPD protocols benefit from using LPDFi narrative.

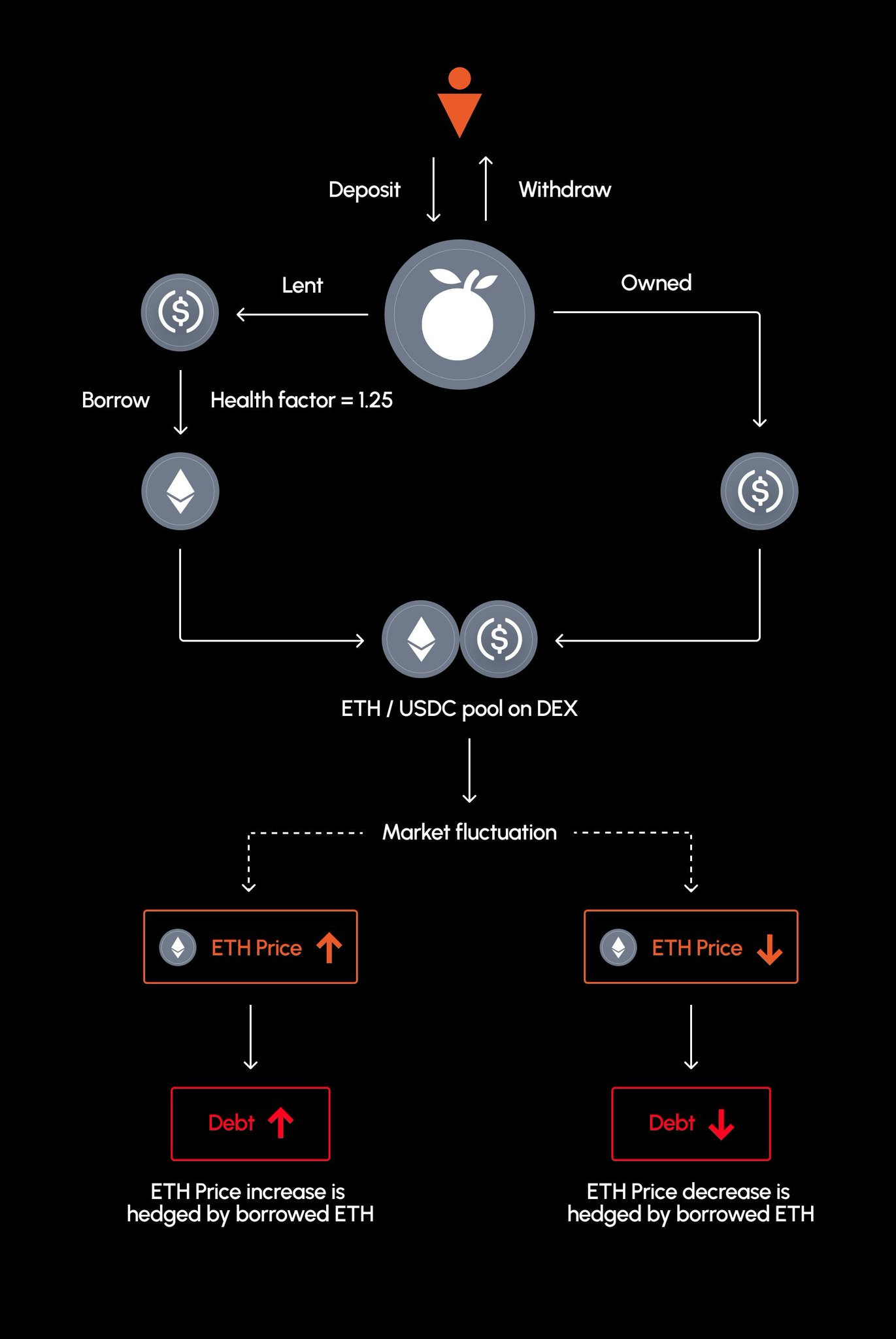

Orange Finance

Orange is a liquidity management protocol with sophisticated hedging strategies designed for Uniswap v3 and Camelot V3. It enables any investor to generate income on DEX (decentralized exchanges). Specifically, Orange utilizes delta hedging to neutralize volatile price movements of assets, safeguarding liquidity providers in the DeFi environment.

In addition, Orange features the Smart Liquidity module, which determines the price range for liquidity provisioning on behalf of liquidity providers and adjusts fee levels based on market conditions. The price range is established by modeling volatility using statistical and financial models such as the GARCH model, considering parameters like implied volatility and historical volatility. Also unique is that Orange Finance's vaults have a hedging module that implements a delta hedging strategy.

Orange LP ERC20 tokens can be utilized for liquidity mining, incentivizing holders to provide concentrated liquidity within specific price ranges and receive greater incentives.

GammaSwap

Unlike other AMMs, GammaSwap is a two-sided market. This means that users can both "buy" and "sell" volatility, opening up new trading strategies and potentially offering more fair volatility prices. Like Smilee, GammaSwap allows users providing LP on external AMMs to hedge against IL by trading volatility. When a perpetual position is opened, GammaSwap burns LP tokens and holds the underlying tokens on the platform. Price movement actually outpaces position collateral since the underlying tokens are now worth more than the LP tokens due to the impermanent loss.

Here's how it works in simple terms:

Liquidity providers will offer liquidity to Constant Function Market Maker (CFMM) just like they do currently, with the difference being that they will provide it through GammaSwap. In other words, LPs will send their tokens to GammaSwap, which will place them in CFMM (e.g., Uniswap, Pancakeswap, etc.) in exchange for LP tokens. Thus, the GammaSwap Protocol consolidates liquidity tokens from popular CFMMs (but not the liquidity itself!) so that they can be lent to other users.

However, these LP tokens from other CFMMs cannot be provided to a liquidity provider, for example, shorting on Gamma. Instead, they remain in GammaSwap. GammaSwap then issues its own liquidity pool tokens, identical to CFMM liquidity pool tokens, such as Uniswap LP tokens (e.g., ERC-20 tokens), representing the liquidity provider's share in the CFMM liquidity pool (these are called reserve tokens).

In the case of longing, reserve tokens are held as collateral, and the user receives a credit. The impermanent losses experienced by the creditors become an impermanent liquidity acquisition for the borrowers.

Thus, the incentive to provide liquidity on GammaSwap is that users achieve increased returns from their LP positions.

Panoptic

In short, Panoptic utilizes Uniswap V3 LP to provide liquidity to both buyers and sellers of options, earning commissions for returning to these credit assets in the Panoptic pool. That is, unlike the protocols described above, Panoptic applies the logic of call and put options, with the accrual of premiums, etc. It is geared towards Perps, enabling trading of put and call options with leverage up to 10x.

Options are a type of derivative. They allow you to speculate on the price level of the underlying asset without actually impacting the asset itself. You can either take a long position by buying call options or take a short position by buying put options. You purchase an option at a specific strike price (i.e., a fixed price at which the option holder can buy or sell the underlying security or commodity) and pay a "premium" (i.e., the market price of the option) to the option seller.

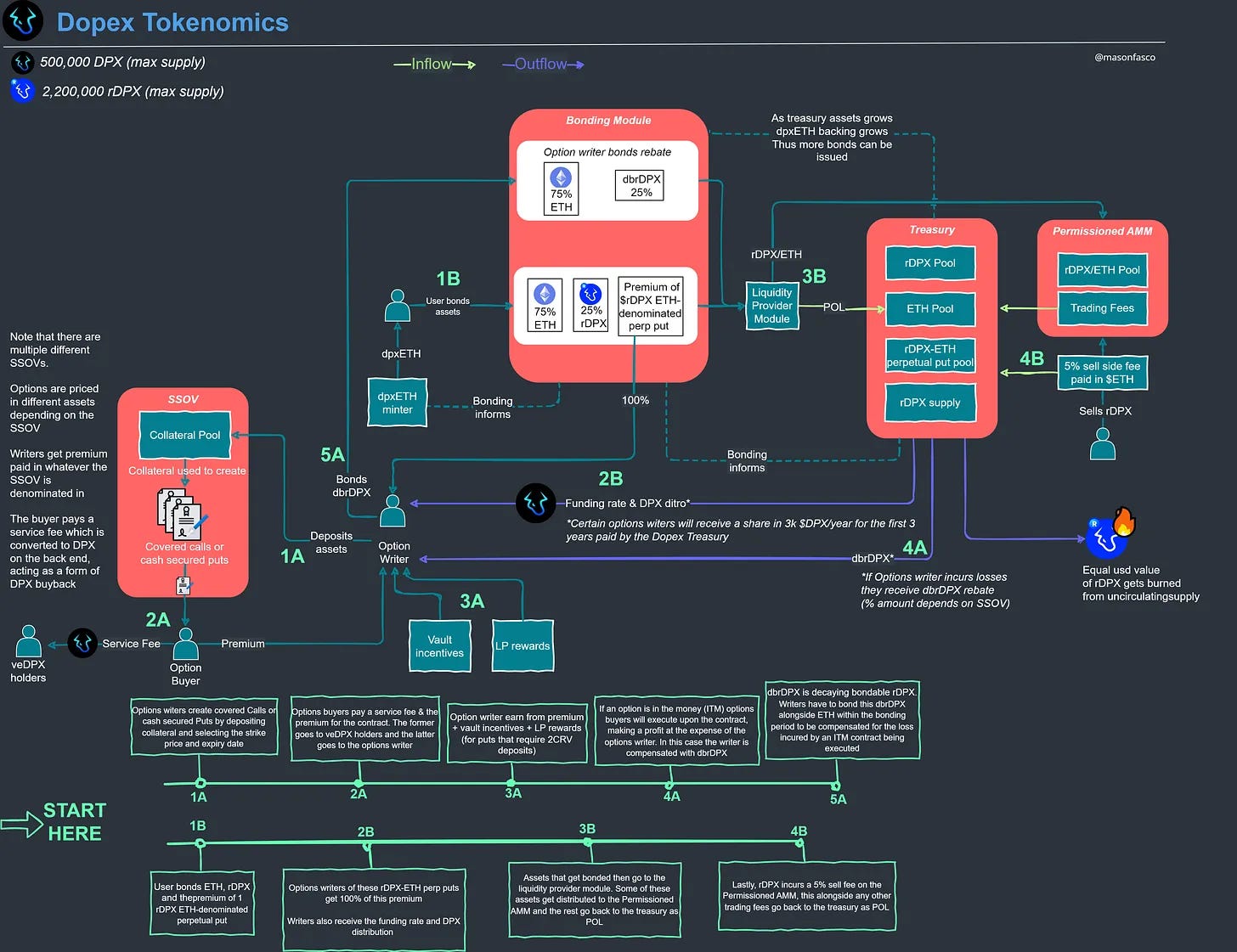

Dopex

Dopex is reminiscent of Panoptic, as it also deals with options, but with a broader range of option products. It is one of the first options protocols on Arbitrum.

The Dopex team has created a unified staking options vault (SSOV) to ensure that losses for option authors are minimized, while option buyers have access to high liquidity and fair prices. The SSOV governance will last for one month. During this time, the option author can deposit an asset, choose the strike price, and then sell the asset to offer a call option at a specific price before it expires.

The Single Staking Options Vault (SSOV) is at the core of the Dopex protocol. A traditional single staking vault, such as Yearn or Abracadabra Degenbox, allows users to deposit one base token and then deploy their capital to generate returns using a strategy or a combination of strategies. SSOV accomplishes this using options as the yield-generating strategy.

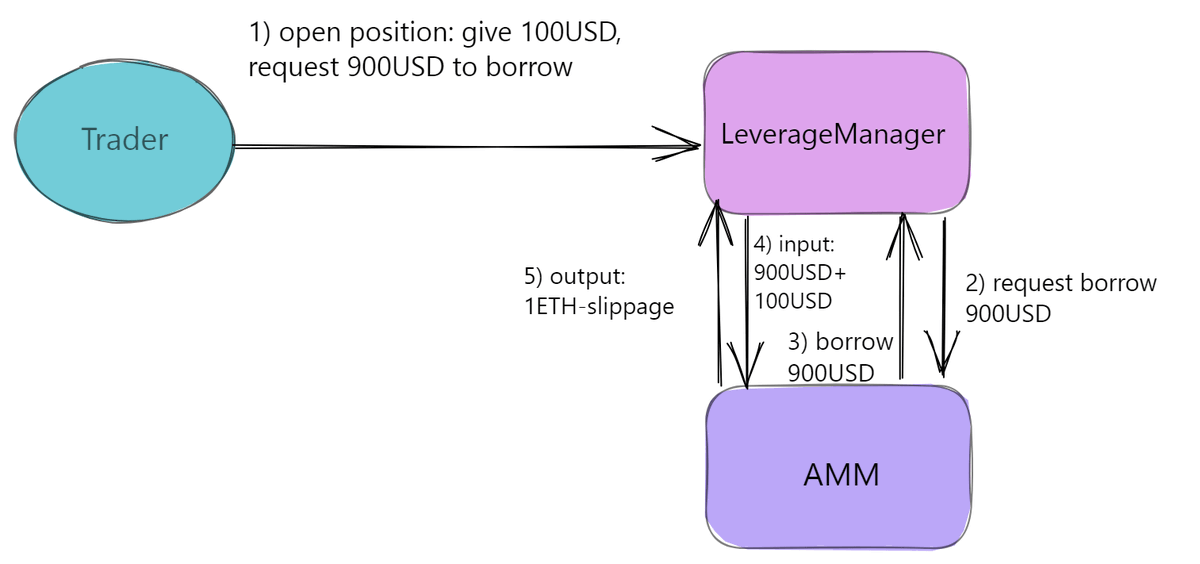

InfinityPools

InfinityPools is a protocol with unlimited leverage and no liquidations or oracles. The protocol is built on Uniswap V3 with concentrated liquidity. At a high level, the protocol operates by DEX liquidity providers (LPs) depositing their LP tokens into the protocol, which are then aggregated and borrowed by traders seeking leverage. Leverage (credit) is generated by utilizing a portion of the underlying LP assets to purchase more assets for the trader on leverage.

By utilizing the LP position as a source of credit, the repayment of the credit can be made with any of the LP assets, eliminating the traditional cash constraint. For instance, if a trader uses a long ETH leverage, and the price moves against the position, the composition of the underlying LP position will change to fully ETH, which the trader will pay off from their position. As a result, leveraged assets do not need to be sold in the market to repay the credit. Thus, the liquidity needed for liquidation, is inherently embedded in the credit source itself (the LP position).

Limitless Finance

Limitless Finance is an liquidation-free and permissionless leverage instrument built on Uniswap V3 without oracles. It combines spot and credit liquidity within a single architecture, reducing liquidity fragmentation between trading and borrowing. Moreover, the Limitless protocol revolutionizes access to leverage for any digital asset, making it accessible to everyone. It blends Uniswap V3 Concentrated-Liquidity Automated-Market-Maker (CL-AMM) technology with a lending mechanism, creating the mechanism of Limitless Leverage Finance (LLF).

With Limitless, liquidity providers on Uniswap V3 can offer liquidity when LP positions go beyond the trading price range (idle LP), in exchange for premiums from borrowers and traders. Meanwhile, borrowers can take high LTV (Loan-to-Value) loans and avoid liquidation risks, while traders can utilize leverage up to x1000 for their trading positions.

3. Market Impact

The main LPD protocols the market currently have or will have in the near future are Panoptic, Smilee Finance, InfinityPools Finance, and Limitless Finance. Let’s do a quick overview of how they work and operate with different types of derivatives.

Panoptic: protocol enables the minting, trading, and market-making of perpetual put and call options. So it’s basically an app built on derivatives. Panoptic protocol uses Liquidity Provider (LP) positions in Uniswap v3 as a fundamental building block for trading long and short options.

Smilee: building on-chain derivatives enabling volatility trading at scale with the Decentralized Volatility Product. DVPs are vault-based strategies that generate payoffs which are either long volatility or short volatility. You can deposit LP tokens earning the DEX APY + a premium.

InfinityPools: offering unlimited leverage on any asset, with no liquidations, no counterparty risk & no oracles. Liquidity providers generate yield from two different sources: spot trading fees and lending out liquidity, so you can basically provide liquidity to its spot AMM.

Limitless: liquidation-free and permissionless lending facility and margin trading DEX built on top of Uniswap V3.

So, with LPDfi protocols and Logarithm in particular you’re able to earn the multiple types of yields at the same time, there’s 4 different types of yield you can earn while interacting with Nautilus Vault:

LP fees from Uniswap V3 (all LPDs are built on Uniswap V3)

LP fees from LPD Protocol (Panoptic, Smiles, Limitless, etc)

Incentives for LPs in $LOG

Token emissions from LPD Protocol

Conclusion

We have outlined the evolution of derivative instruments in DeFi, beginning with classic derivatives that allow leverage and culminating in a liquidity layer facilitating various types of yield. Also, as you may have noticed, LPDFi protocols are currently very difficult to describe in 1-2 sentences due to their complex mechanisms. And at the moment it will be quite difficult for an ordinary user, who is not sophisticated in DeFi, to understand the strategies and principles of such protocols. In addition, most protocols in LPDFi (that deal with options) have a direct correlation: the more traders - the more returns - the more the project can create incentives and attract even more users and liquidity. The exact opposite is also true.

Therefore, most likely, we should expect a new round of LPDFi development in the direction of increasing usability and yield. Soon, we will publish an article providing detailed insights about our portfolio company, Smilee Finance, as a part of the LPDFi Ecosystem, which is a project from this complex category, but pays much attention to UI/UX and accessibility for users.

Our links:

🔗 Website

🐦 Twitter

✉️ Substack

🔸DeBank

🐰 Friend.tech